Testimony to Senate Finance Committee and Assembly Ways and Means Committee:

FY 2021 Executive Budget: Economic Development, Taxation and Other Business Issues

My name is Ken Pokalsky and I am Vice President of The Business Council of New York State, Inc. We are New York’s largest statewide employer association, representing 2,200 private sector employers across New York, in all major business sectors.

As always, we appreciate this opportunity to address members of the Senate Finance and Assembly Ways and Means Committee on the Executive Budget.

In our testimony today, we address the major business climate and business regulatory issues presented in the FY 2021 Executive Budget, including economic development programs, taxation, workforce development issues and others, including business climate issues and sector-specific proposals with a significant potential impact on private sector employers and jobs.

Overview

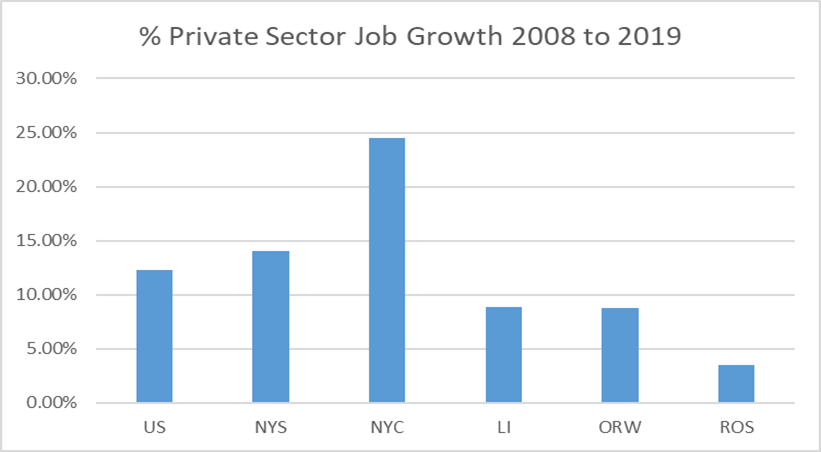

While New York State’s economy overall is doing well, with an all-time high number of private sector jobs at the end of 2019, and overall job growth exceeding national levels, much of the growth has occurred in and near New York City. As shown in Chart 1, “upstate” has seen private sector job growth, since 2008 pre-recession levels, at a rate about one-seventh of that enjoyed in New York City (3.4% versus 24.4%). The suburban counties to the north of the city, and Long Island, also had significantly greater job growth than upstate, although well below New York City’s levels, and slightly below the national job growth rate as well. Further, even though New York State’s cumulative post-recession job growth is still greater than the nation’s, the U.S. private sector job growth rate has exceeded New York’s in each of the past five year.

Low – even “historic low” – unemployment rates mask the underlying economic reality in many parts of upstate New York. In several upstate counties, low unemployment rates are a function of a declining workforce, rather than robust job growth, as their job growth levels remains sluggish, or even negative.

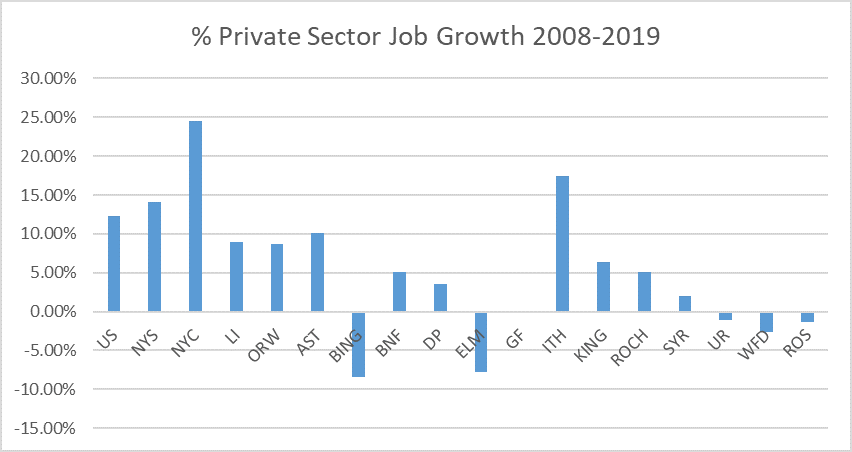

Of course, there are significant regional differences across upstate as well, as shown in Chart 2. Several upstate areas, including the Capital Region and Tomkins county, have done well. However, at the end of 2019, several other Upstate labor markets – Binghamton, Elmira, Glens Falls, Utica/Rome, Watertown – are still at or below their 2008 pre-recession job levels, and the rural counties that fall outside of these urban labor markets collectively are below 2008 job levels as well. Other than the Capital Region, the major upstate urban areas have growth rates less than half the national average.

We urge you to consider these trends as you review legislation that may impact individual businesses or the state’s overall business climate. The Business Council provides support for the Siena Research Institute’s annual survey of Upstate Business CEOs, and its recently released 2020 survey shows that upstate business leaders are increasingly concerned about the state’s economic competitiveness, and their own ability to survive let alone continue to invest and grown. And, importantly, they point to state-imposed “headwinds” – including labor law mandates and other regulatory requirements and state-imposed costs – as adding to their challenges.

Against this backdrop of recent economic trends across New York State, we would like to address several of the most significant business and business climate issues presented in the FY 2021 Executive Budget.

Taxation

The Business Council has supported Governor Cuomo’s overall approach to fiscal management, which is reflected in relatively low year-to-year growth in state spending. This spending restraint has allowed for both middle class personal income tax reductions and the reform and reduction of some business taxes. We also applaud your recent permanent extension of the real property tax cap, which has saved taxpayers overall an estimated $38 billion since its enactment, including as much as 20 percent of that for business taxpayers. We also appreciate legislation approved at the end of the 2019 session to decouple from federal TCJA provisions that would have resulted in unintended tax increases on business. The legislature also approved important personal income and business tax decoupling legislation in 2018.

Small Business Tax Reform – We welcome the Executive Budget inclusion of small business tax reform, although we are concerned with its limited scope, especially for non-incorporated businesses whose owners pay tax on business income under the personal income tax (PIT). In the budget proposal, the PIT component of this tax reform is limited to sole proprietors. In contrast, in the FY 2017 Executive Budget, a similar tax reform was proposed for all small businesses regardless of their legal structure, including partnerships, limited liability companies, sub-S corporations as well

as sole proprietorships. That year, the Senate and Assembly also both endorsed small business tax packages similar but not identical to the Governor’s proposal in their respective one-house budget resolutions. Unfortunately, a compromise measure was not included in the final budget agreement. We recommend that the legislature consider broader small business tax relief, as proposed in 2016. Given its past bipartisan support, a similar small business tax reform legislation should be achievable as part of the FY 2021 state budget.

Small Manufacturers Tax Relief – The Senate and Assembly should also consider incorporating into the final budget another pending small business-oriented tax provisions, S.4671 (Kaplan) / A.636 (Stirpe), that would provide a state personal income tax exemption for income earned by a “qualified pass-through manufacture.” This legislation completes Governor Cuomo’s 2014 initiative to cut business income taxes for New York manufacturers, which reduced the “entire net income” based corporate franchise tax rate for manufacturers to zero. This legislation has the same effect for manufacturers organized as partnerships, LLCs, s-corporations or sole proprietorship – commonly referred to as “pass-through entities” as their income is “passed through” to their owners and taxed under the personal income tax.

Manufacturing firms are extremely valuable to the State’s economy. They provide relatively high wages – statewide, manufacturing jobs pay nearly $15,000 more in wages than the average private sector non-manufacturing job. They provide a significant share of all private sector wages in many parts of the state – manufacturing jobs provide more than 20 percent of all private sector in twenty-three counties, and more than 15 percent in thirty-six counties. And manufacturing activity has a high multiplier effect, positively influencing jobs and economic activity in the surrounding area. (Our November 2018 report on the state of New York’s manufacturing sector is available here). Even so, as U.S. manufacturing employment increased by more than 10 percent since 2010, New York has continued to lose industrial jobs, another 14,000 or 3 percent of its 2010 total.

This legislation will reduce state-imposed costs on smaller manufacturing firms across New York State. Its direct cost to the state is estimated at less than $50 million annually. However, a recent study conducted by The Beacon Hill Institute estimated that "the elimination of the PIT for pass-through manufacturers would increase private sector jobs by 3,455 the first full-year and by 4,850 in 2022. The increase in economic activity sparked by extending the zero-percent tax rate to income from pass-through manufacturers would mitigate the loss of revenue to New York State and boost local tax collections.

TCJA Decoupling – New York, like many states, passed legislation to avoid unintended state-level tax increases resulting from the state’s tax law automatically reflecting provisions of federal law changed by the federal “Tax Cut and Jobs Act,” or TCJA. In the FY 2019 state budget, New York approved several major “decoupling” provisions under both personal income and business tax statutes. Likewise, in the FY 2020 budget, the legislature approved several additional measures, and later in the 2019 session the legislature approved a decoupling measure for “global intangible low taxed income” under the corporate franchise and insurance tax laws. However, several significant issues still need to be addressed:

- An exemption for “global intangible low taxed income” under the New York City corporation tax. Legislation was approved in 2019 providing an exemption under the state’s corporate franchise and insurance tax, but the city’s corporation tax was left out of the final agreement. Most states are or have decoupled from this federal change, as have other cities, such as Philadelphia, that have their own business tax statute. GILTI is a calculated attribute of foreign income, and represents net income that has not yet, and may never be, remitted to the U.S. taxpayer. It should not be subject to tax at the state or local level.

- Decoupling from the TCJA’s cap on the deduction of business interest expenses at 30 percent of business income, which was included in the federal law, but offset by a five-year period in which business could immediately deduct (or expense) rather than depreciate, most capital investments. New York is already decoupled from federal bonus depreciation, but New York business taxpayers will be subjected to higher state tax liability due to the state’s automatic acceptance of the interest deduction cap, which will even apply to expenses related to capital investments made before adoption of TCJA. New York should decouple from the federal cap. So far, businesses in seventeen states are exempt from this provision, including eight that proactively decoupled (CT, GA, IN, MO, SC, TN, VA and WS), three – including California, that unlike New York do not automatically incorporate federal language changes, and six others that have no statewide corporate income tax. This issue is addressed in S.7029 (Benjamin) / A.5961-A (Schimminger).

In general, the state had projected limited additional revenues from these provisions, so amendments adopted in the 2020 session should not adversely impact the state’s long-term financial plans. However, these conformity issues will be an economic competitiveness issue for New York and other states. Given the Administration and legislature’s focus on avoiding unintended tax increases due to TCJA, these issues should also be addressed during the 2020 budget process.

Economic Development Programs and Business Climate Issues

Expansion of Prevailing Wage – We remain strongly opposed to legislation to extend the public works’ prevailing wage mandate to private sector projects receiving state and/or local economic development assistances. These measures are simply contrary to the state’s economic development objectives, adding significant additional costs and regulatory obligations to projects recognized as needing assistance to move forward. This concern is especially true in upstate where many counties have seen flat economic growth. Driving up project labor costs will hamper a wide range of investment and job creation projects, including those sponsored by for-profit businesses as well as non-profit service providers on which our communities rely. Comparing total mandated prevailing wages and supplemental benefits to actual average wages for specific construction occupations in upstate labor regions shows differentials rarely under forty percent, and as high as 100 percent or more.

We recognize that the Executive Budget proposal (S.7508 / A.9508, Part FFF) is more limited than other pending legislation, in several significant ways. It would impose the prevailing wage mandate only on those projects valued at $5 million or more where public assistance is at least 30 percent of project costs. It exempts several specific incentive programs, including those for brownfields, historic preservation, downtown revitalization, affordable housing, and others. It also exempts incentive programs that are primarily intended to support non-construction expenditures, as well as those whose value cannot be calculated at the onset of the project. These final exemptions include, but are not limited to, incentive programs based on job creation.

In addition to our threshold concerns about any prevailing wage expansion into private sector projects, we oppose other provisions of the Executive Budget proposal. It would subject these projects to the state’s Article 15-A MWBE requirements, which were expanded and extended in 2019 without necessary reforms, resulting in the imposition of MWBE participation targets that are unrealistic for some labor regions. It also proposes the creation of a subsidy board which would have expansive, and we believe inappropriate, authority to revise the “covered project” applicability thresholds without having to resort to legislative changes or formal rulemaking.

Mandatory Sick Leave – Based on the broad-based input from our members, we oppose employee leave mandates. Studies show that nearly three out of every four employers in the U.S. already provide paid sick leave to their employees. Employers design and administer these sick leave plans and other employee benefit offerings to meet the unique needs of their employees and customers. Broad legislative mandates rarely meet the needs of the employer or the employee, and in addition to direct costs, also impose challenging administrative burden on employers as well, especially small business. Legislators recognize these inefficiencies and routinely exclude employees of government agencies and certain collective bargaining agreements from such proposals.

We appreciate that the Executive Budget provides an alternative mandate for the state’s smallest employers, requiring unpaid, but job projected, leave for employees of less than five. However, the Executive Budget proposal provides little detail on the key definitions and administrative requirements of this leave mandate. In contrast, New York City’s paid leave mandate, effective in April 2014, imposes an expansive definition of allowable use of leave, and detailed administrative mandates on employers. In fact, data provided by the NYC Division of Consumer Affairs for the for the first three years of their program’s application show that most complaints are for alleged administrative violations, such as notice requirements. This evidence suggests that the administrative requirements of the City’s law are too complex for small businesses that typically do not have a dedicated human resource professional.

Faced with low unemployment and severe workforce shortages, employers of all sizes will be faced with staffing difficulties and administrative burdens if such a law were imposed on the entire state. This one-size fits all approach will continue to increase the cost of doing business in New York State putting continued job growth at risk.

Other Executive Budget Provisions

The Executive Budget contains numerous other provisions of interest or concern to our diverse membership. We will address several of the more significant ones here.

We support:

- CPA Ownership –This provision allows public accounting firms to incorporate in New York State with minority ownership by individuals who are not Certified Public Accountants, provided the words "Certified Public Accountant" or the abbreviation "CPA" is excluded from the firm's name (S.7506 / A.9506, Part G). Similar legislation is in place in at least forty-seven states, and this proposal has passed the Senate in each of the last six years with broad, bipartisan support (four times unanimously). However, it been prevented from being brought to the Assembly floor. We are aware of no organized opposition. It should be given two-house approval in 2020.

- Workplace Impairment Provisions regarding Cannabis – The Business Council has taken no position on the threshold public policy issue of legalization of recreational use of cannabis. However, we have been concerned that earlier proposals would place a significant burden on employers to demonstrate the employee’s impairment as a result of the use of cannabis that goes well beyond what is required regarding other intoxicating substances. As a result, such language would compromise an employer’s obligation to maintain a workplace free from hazards, impairing the safety and well-being of employees and customers alike. Both New York State occupational safety laws and the Federal Occupational Safety and Health Act require employers to maintain a safe and healthful workplace free from recognized hazards. This year, the Article VII proposal (S.7509 / A.9509, Part BB, proposed §127(4)) preserves key workplace safety mechanisms for employers. It allows employers to implement policies prohibiting the use or possession of cannabis during work, and to take disciplinary or adverse employment action against an employee for violating an established workplace policy or if the results of a drug test administered in accordance with applicable state and local law demonstrate that the employee was impaired by or under the influence of cannabis while in the workplace or during the performance of work. We strongly support this Executive Budget language. Our one recommendation, in recognition of the current tension with federal law, we recommend the following sentence be added to Section 127, Paragraph 6: “This subdivision shall not require any person or entity to do any act that would put the person or entity indirect violation of federal law or cause it to lose a federal contract or funding.”

- Meaningful Career and College Preparedness – We support several provisions of S.7503 / A.9503 related to career and college readiness. These include $5.8 million in proposed funding to subsidize the costs of AP and IB exam fees for low-income students. This investment has been attributed to New York seeing an increase of low-income test taking by 11.7 percent, compared to the national average of 1.6 percent. A small increase in funding, just $500,000, will maintain last year’s charge of just $5 per exam. In addition, we have been ardent supporters of the more than 90 early college high school programs across the state, which are allowing students to get a jump start on college and career training by allowing them to obtain college credits up to an associate degree in high school. We support the proposal for $6 million for new early college high school programs across the state. In addition, we propose setting aside $500,000 of the to fund one or more Technical Assistance Center dedicated to providing necessary program supports and guidance and to act as a professional learning network for these unique programs. This critical investment will support both the long-term success of these individual programs and the ECHS network as a whole.

- “Gig” Worker Study – We welcome the proposal – S.7508 / A.9508, Part GGG – to establish a task force to study the classification of workers in the “gig” economy (i.e. should these workers be considered employees or independent contractors). The Business Council has already provided detailed comments on this issue to both the Senate and Assembly committees that recently held hearings on this subject. We all recognize that the nature of work has changed since the adoption of the National Labor Relations Act of 1935, the Taft-Hartley Act of 1947, and current IRS law regarding the definition of employee. It is important that state and federal labor laws change and adapt in response to the new realities of the nature of work and the desires of workers. Any efforts by New York to address the independent worker issue needs to consider how changes will affect New York’s general business climate, and impact workers whose flexibility could be sharply limited by reclassification. Again, The Business Council urge’s any task force to be innovative and seek a new and creative “third way.” We look forward to participating in the process.

- Annual Rate of Interest on a Judgment or Accrued Claim – We support the provisions in S.7505 / A.9505, Part T, which would calculate the annual rate of interest to be paid on a judgment or accrued claim, at the weekly average one-year constant maturity treasury yield as published by the Board of Governors of the Federal Reserve System for the calendar week preceding the date of entry of the judgment awarding damages. Replacement of the current, excessively high, 9 percent interest rate on judgments in civil lawsuits and replacing it with the prevailing market rate of interest is both logical and fair. Such a change would be good for New York consumers who have had to pay this excessive rate on judgments for years. It would also greatly benefit municipalities throughout the state and concurrently help control insurance rates for all purchasers.

- E-Scooters – This provision (S.7508 / A.9508, Part AAA) would add a new §34-D to the Vehicle and Traffic Law to authorize and govern the use of electric scooters in New York State. Many cities across the country have seen a tremendous growth in this safe, fast and consumer friendly form of transportation. This proposal takes a workable approach to the authorization of this new and growing mode of travel. These proposed provisions allow the use of electric scooters on public highways and private roads with posted speeds not higher than 30 miles per hour, precludes operation on sidewalks, limits maximum speed to 15 miles per hour, requires certain safety features such as lights and bells/audible devices, and authorizes localities to set additional rules and regulations.

We oppose:

- Potential Health Care Assessments – Given the significant funding gap in the state’s Medicaid program – driven primarily by spiraling costs resulting from a handful of specific policy changes, rather than a lack of revenues – The Business Council has joined with a broad group of organizations to urge the Medicaid Redesign Team (MRT) to avoid recommending new or increased taxes on the privately insured to close the funding shortfall in the Medicaid program. While we recognize the current challenge the state faces in addressing the Medicaid deficit, the MRT should focus exclusively on reforming and controlling costs in the Medicaid program, not adding more revenue from the privately insured. A workgroup charged with reassessing the way the program’s current structure is driving unsustainable costs should not undertake policy discussions that will add to the cost of health insurance for New York businesses and the individuals they employ, union benefit funds or individual consumers. Moreover, commercial insurance currently subsidizes health care providers for inadequate Medicaid funding. Any further reduction in Medicaid funding to hospitals will further increase that commercial subsidy. Therefore, taxes of any kind – e.g. HCRA taxes, personal income taxes, corporate taxes – should not be part of the MRT’s directive. New York currently collects more than $5 billion dollars annually through various taxes, surcharges and assessments on health insurance and providers, representing the third largest source of state revenue behind the personal income and sales taxes. These taxes apply to every entity providing coverage including employers, union benefit funds, and the more than 250,000 consumers in the individual market, and amount to well over $1,000 per premiums for the average family receiving health care coverage in New York.

- Expanded DFS Authority – Several Executive Budget provisions expand the reach of the Department of Financial Services (DFS). This expansion of DFS authority is mostly in areas in which DFS has not previously had a role, specifically with entities that are already heavily regulated by federal and state agencies. In S.7508 / A.9508, Part NN, DFS’s authority would be expanded to cover any entity that sells to a consumer or small business, any security, investment advice, or money management device, warranty, guarantee and suretyship, among other services. It also expressly removes language from the Financial Services Law that exempts financial products or services that are regulated under the exclusive jurisdiction of a federal agency or authority, or regulated for the purpose of consumer or investor protection by any other state agency, state department or state public authority. Not only is this expansion of DFS regulatory oversight to already-regulated financial institutions unnecessary and duplicative, federal law preempts state laws, such as this, that interfere with the regulation of national banks. Further, S.7507 / A.9507, Parts G and U give new powers to DFS to regulate the price of pharmaceuticals as well as regulating pharmaceutical benefit managers. These provisions all have one thing in common. They all unnecessarily increase the regulatory burden on employers and will inevitably further drive up the costs of doing business in the state. Unfortunately, there are many other proposed measures that would either directly raise the cost of health insurance premiums or indirectly do the same. The laundry list of provisions in S.7507 / A.9507, Part J for instance, will make it all but impossible for health insurers to combat fraud and control costs.

- Freshwater Wetlands Program – We support efforts to update New York’s wetlands statute, but in a way that would recognize the needs of landowners, in addition to assuring the protection for valuable ecological resources. However simply eliminating the current mapping requirements, and the corresponding right for the public to be notified and make substantive contributions to the process, as proposed in S.7508 / A.9508, Part TT, is the wrong approach. This proposal would create significant uncertainty for residential and commercial property owners and developers by eliminating the determinative effect of wetland maps. It will also impose additional uncertainty and administrative burdens on state regulators who would be tasked with determining on a case-by-case basis what is or is not a protected wetland. We are not opposed to updating New York’s wetlands statute. But it should be done in a way that recognizes the current protections that are afforded wetlands by State and Federal laws, regulations, and guidance, and the need to provide regulatory certainty to property owners; not through adding ambiguity as would be the case under this proposal.

- CAT and COE Funding – We opposes S.7508 / A.9508, Part BBB which would consolidate the Centers of Advanced Technology (CAT) and the Centers of Excellence (COE) programs by repealing the “Centers of Excellence” program; allow COEs to apply for designation as CATs; reduce the total program funding to $19.5 million, a reduction of $7.2 million; and create a competitive funding program for all centers. This proposal is intended to allow the state to better capitalize on the Centers with the highest performance, but it instead restricts all programs ability to operate and innovate by significantly reducing their funding. These Centers employ industry experts and highly specialized research scientists in order to execute the innovative partnerships with industry. This significant reduction of funding will have a direct impact on staffing resources. The universities and research centers that have COE and CAT centers greatly benefit by having access to this highly educated and skilled talent, and their loss would be felt throughout the university. In their annual reporting on the CAT and COE programs, Empire State Development Corporation (ESDC) estimates non-job-related economic impacts for 2017-2019 to amount to $2.57 billion, resulting in an annual return on investment ranging from 25:1 to 45:1. ESDC’s reporting demonstrates that CATs and COEs are among the best programs the State has for job creation and economic growth. These Centers are a tremendous asset to the innovation ecosystem in New York State and reducing this program would further diminish New York’s economic development competitiveness and vitality.

- “Pink Tax” – We oppose this proposal – S.7508 / A.9508, Part S – that would prohibit different sale prices for “substantially similar” consumer products and services if the pricing differences are: for products, based on the gender of the persons for whom the products are marketed and intended; or for services, if such services are priced differently based upon the gender of the individuals for whom the services are performed. The bill gives enforcement power to the state Attorney General, but also creates a private right of actions to enjoin violations and recover the greater of $50 or actual damages, with the option of a treble damage assessments up to $1000. The bill is of questionable need or value from a consumer protection perspective. Even if two “substantially similar” products are priced differently based on marketing considerations, consumers are obviously able to select which they purchase, and decide for themselves whether a specific product is worth any price premium. In addition, the proposed standard for assessing “violations” is “substantially similar,” an incredibly imprecise standard that will lead to significant enforcement discretion, and broad opportunities for private legal actions that, regardless of their merit, will impose significant legal costs on business. The bill recognized that many factors influence the price charged for goods and services, including but not limited to “the amount of time, difficulty or cost incurred in manufacturing such products or offering such services.” This legislation could result in manufacturers and retailers having to repeatedly demonstrate how such factors were considered in setting the price for consumer products or services, and to demonstrate how such factors result in a “legally excusable differences” in the eyes of the Attorney General or the courts.

- Comprehensive Technology Service Contracts – Our concern with the multiple provisions of S.7505 / A.9505, Part X focuses on its proposed Section 103.22 (c) that would require every state technology contract to include onerous payment claw back and cost assessment requirements that would apply in certain cost overrun circumstances. While we are still reviewing this language with our major IT companies, we expect that if adopted it would be a powerful disincentive to bidding on state IT contracts. We believe that more measured provisions can be negotiated.

- Ban of Polystyrene Containers and Packaging – This provision – S.7508 / A.9508, Part PP – would impose a statewide ban on the sale and use of disposable polystyrene food containers by food service providers, with limited exemptions. It also gives the Department of Environmental Conservation broad authority to adopt “regulations to limit the sale, use, or distribution of” any other packaging products it determines to have “environmental impacts.” At a time when the state legislature should be considering approaches to improve the state’s business climate, particularly in upstate regions, this legislation would ban the principal product at least ten upstate manufacturing plants, employing 2,000 individuals.

- Sexual Harassment Reporting by State Contractors – We oppose this provision – S.7505 / A.9505, Part BB – that would mandate that vendors doing business with New York State, or those bidding on state contracts, provide written proof of compliance with sexual harassment training and a detailed history of how past cases, including court cases and settlements, have been handled by vendors. As a practical matter, it is unclear why vendors and bidders should be subject to a higher legal standard than is applied to employers in general under the state’s anti-harassment policy, training and response requirements. Also, this proposal goes way beyond the workforce, or even the business unit, engaged in state bidding to require reporting on a bidder’s total business activities. This legislation would require a significant amount of time and effort to compile information that is extraneous to the delivery of goods and services, and imposes additional requirements on state agencies to collect, process and compile yet another state report. Given the recently enacted expansion of the state’s anti-sexual harassment laws, and new policy, training and response obligations imposed on all New York State employers, we question the need for this additional layer of reporting.

- Net Neutrality – This provision – S.7508 / A.9508, Part AA – would amend the Public Service Law by creating a new §12 regulating internet service providers to establish a so-called net neutrality system in New York State. The regulation of the internet properly belongs under federal oversight through the Federal Communications Commission (FCC). Our members remain steadfast in their support for an open internet, including reasonable federal protections to address practices that would threaten it. The internet is not limited by state boundaries nor are e-commerce markets. Both consumers and providers should be governed by a unified federal standard. Following the Federal Communications Commission’s (FCC) order “Restoring Internet Freedom” in 2018, FCC rules require providers to be transparent about their practices. The Federal Trade Commission (FTC) was empowered to investigate and pursue any conduct that threatens consumers, as well as competition that is deceptive without discouraging competition and slowing job-generating investments. This restoration overturned a previous ruling by the FCC in 2015 that had imposed a 1930s system of regulations (“Title II”) that led to limited investments and a decrease (according to the FCC) in network broadband investments. The FTC will also provide a single national framework that will apply to all providers and Internet companies, giving consumers nationwide consistent and fair protections. In its wake, nationwide internet service has maintained broad access and high consumer satisfaction, contrary to some advocates' claims of likely widespread adverse impact on users. This bill would contribute to a system of annual certification in New York State, creates state definition of “net neutrality,” and numerous state-level rules on content service. The act is enforceable by the Attorney General but also adds a private right of action all but guaranteeing an expansion of court cases on this untried field of state regulation of the internet.

- Department of Public Service Enforcement Authority – We oppose Part Z of S.7508 / A.9508, which proposes to vastly expand the scope of authority vested in the Department of Public Service (DPS). Under current law, the Public Service Commission has broad oversight and enforcement authority. To commence a formal proceeding, the PSC would issue an “Order to Show Cause”, which requires a combination gas and electric utility to publicly respond to the allegations levied against it. Part Z represents a significant change to the current statutory framework, allowing rather than the Commission, to initiate proceedings against a combination gas and electric corporation, or an electric corporation, gas corporation, a cable television corporation, and/or a telephone corporation. It removes the requirement that a ‘order to show cause’ be publicly issued to begin a formal investigation. The result is a process that would be less transparent and more likely to be used punitively against entities disfavored by a given administration for any number of factors. We believe the state’s broad enforcement authority should remain the function of the independent Commission, rather than Department staff.

- Contributions by Foreign Controlled Corporations – We oppose yet another proposed restriction on the participation in political advocacy by incorporated entities. This language – S.7505 / A.9505, Part SS – would prohibit campaign contributions and indirect expenditures by corporations that have either: a single foreign national with 5 percent or more control or ownership of the company; two or more foreign nationals with ten percent or more, in aggregate, control or ownership; or has any foreign nationals participating, directly or indirectly, in the company's decision-making process as it relates to political activities in the United States. The Executive Budget bill memo provides almost no justification for this proposal. It seems unreasonable to say that these levels of limited foreign ownership of a publicly traded company will lead to political expenditures that are somehow contrary to the state (or national) public interest. The state already severely limits corporate political spending (to $5,000 annually), and limits mechanisms for contributions to employee PACs in ways not applicable to other categories of PACs. We oppose this provision as merely more of the same one-handed campaign finance “reform.”

- “Robocalls” – This provision – S.7508 / A.9508, Part T – would amend the General Business Law to address the issue of robocalls at the state level partly by mandating telephone service providers to offer free call mitigation technology to telephone customers. This language, while well intended, fails to take into consideration that action is underway at the federal level to address this very issue. The Federal TRACED Act, enacted December 30, 2019, already addresses the issue at the national level. The TRACED Act requires the FCC to undertake over two dozen regulatory proceedings and other agency actions covering a broad range of issues, particularly robocalls. Because of the firm statutory deadlines, key industry and governmental stakeholders at all levels (including the state) will be fully engaged in a wide range of robocall and fraudulent call mitigation efforts. This initiative – not new state programs – will best serve as the effective consumer friendly, board-based, nation-wide effort to attack the problem of robocalls.

Thank you again for the opportunity to testify today, and I welcome any questions or comments you have on these or other tax policy issues.

#